The FOS and FCA have begun a journey on modernising the redress system, issuing a call for input which closed in January 2025, with next steps for implementation targeted for 30 June 2025 (There are no new updates on the FCA website at the time of publishing).

The current redress framework, while being seen to work well for individual customer complaints about specific issues has been cited as falling down on systematic issues and mass redress events in particular.

Most recently, the impact of the uncertainty around possible outcomes from the current FCA motor finance review has negatively impacted the share values of those lenders most exposed in the sector. Additionally, the requirements for further capital provisioning has been identified as a key contributor to stalled innovation and investment in the sector.

In November, the Chancellor announced in her first Mansion House speech her aim to modernise the UK’s financial redress system, particularly through the Financial Ombudsman Service (FOS) and Financial Conduct Authority (FCA). The objective being to address concerns that the current system creates uncertainty for financial firms, muting appetite for investment, while still seeking to balance consumer protection with industry stability.

The Data

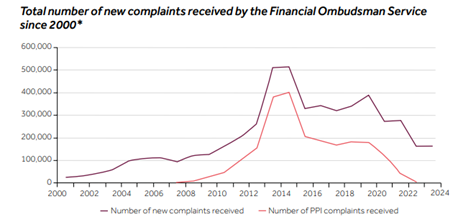

According to the FOS website, they received 141,846 new complaints between 1 July and 31 December 2024, an increase of 49% compared to the same period in 2023, when they received 95,349 complaints.

Of these new complaints, 109,155 were in the banking and credit sector, compared to 62,139 in the second half of 2023.

As stated in the Treasury Committee meeting on 11 February 2025, the FOS was, at that time, working through a caseload of 60,000 relating to motor finance commission.

Impact of Professional Representatives (PRs) and Claims Management Companies (CMCs)

PRs and CMCs are once again in the crosshairs, having previously been a focus of the Jackson reforms some 10 years ago. Once again, their charging practices are in question, along with their general role in exacerbating the challenges of mass redress events in particular.

As of 1 April, the FOS plans to implement a case fee of £250 for professional representatives and CMCs, in a move aimed at discouraging frivolous, poorly articulated and speculative complaints.

Misalignment between FCA and FOS

This joint FCA and FOS call for input proposes changes primarily aimed at addressing mass redress events, removing inconsistencies, accelerating decision-making, and providing greater clarity on expectations for firms.

As per comments made in the Parliamentary Committee discussion, this failure stems from the inherent design of the FOS process, which is relatively informal and requires the FOS to ‘take into account’ (but not necessarily follow) relevant law and regulations, regulators’ rules, guidance and standards, codes of practice and (if relevant) what the FOS considers to have been good industry practice at the relevant time.

The reforms propose empowering the FCA to override FOS decisions in significant cases, allowing the FCA to implement industry-wide redress schemes or redirect cases to courts for more rigorous adjudication. This could reduce the FOS’s role in shaping regulatory policy, which some argue exceeds its original mandate.

Early identification

Earlier identification of mass action redress is targeted, with the onus placed on the FCA to determine where issues of wider implications exist, based on it being better placed to spot such thematic events rather than firms.

Comparisons have been made to the US model, which is rules-based, rather than the UK’s principles based system, which leaves room for ambiguity in the interpretation of those principles.

Proposals have been put forward for firms to both identify harm at an early stage, proactively address it, and resolve complaints more effectively themselves, with calls for a two-stage internal dispute resolution process, rather than the current single-stage process. This will serve to reduce the need for consumers to refer complaints to the FOS to receive a fair outcome.

A two-stage process was previously in place but was abolished in 2011, as it was prone to misuse, incentivising some firms to deal with complaints to a lower standard at the first stage, knowing that relatively few consumers would pursue them further. It is now being reconsidered given the consumer duty framework already in place, which should allow for better customer outcomes.

Time barring

New time limits for complaints aim to balance consumer access to redress with firm certainty by encouraging prompt complaint filing while reducing the burden of historic claims. A key proposal to meet this objective is the introduction of a ‘longstop’, similar to that used in civil claims.

Currently, consumers have six years from the event, or three years from when they became aware of the issue if later, to bring a complaint, and six months to refer it to the FOS after receiving the firm’s final response. However, this system relies on consumer knowledge and with some products, such as pensions, misconduct may take longer to manifest.

A proposal has been made to introduce a ‘longstop’ to give firms greater certainty and to add limitation to their liability for unsuitable advice provided many years ago.

What’s next

This all sounds promising for customers, firms and UK plc and efficiencies can only be a good thing can’t they?

The next steps for implementing changes were due to be published on 30 June 2025, so we will see what makes it through.

While efficiency and predictability are the key themes, it seems more onus could be placed on firms to support the drive for timely and good outcomes, building on the requirements under the Consumer Duty framework. For those that don’t manage to deliver, we could well see a more empowered regulator coming down very hard on them indeed.

Baroness Manzoor, acting in her capacity as the Chair of the Financial Ombudsman Service, commented in the Treasury Committee meeting of February this year: “let us do something radical guys, if we do not, what is the point?

Insurance implications

As with all key regulatory changes, it will take time for firms to navigate the impact on their business and raise the bar on their internal governance and reporting accordingly.

While the underlying theme is to promote faster, fairer outcomes for consumers in addition to encouraging investment in the UK economy, we can expect increased investigations and regulatory actions for firms that are seen to fail to meet such obligations.

We may also see increased litigation in response to a firm’s failures to meet redress obligations, in a move to reduce the burden on an under-resourced ombudsman service.

Insurers are likely to pay very close attention to their risk selection, anticipating that D&O and PI policies may respond more quickly and at greater cost.

We also expect to see brokers paying closer attention to the claims offering of capacity providers.

-

Oliver Hussey

Product Specialist - Financial Institutions

https://committees.parliament.uk/oralevidence/15379/pdf/

https://www.fca.org.uk/publication/call-for-input/call-for-input-modernising-redress-system.pdf